DCF and Reverse DCF – A New Lens for Valuing Stocks

It’s far better to buy a wonderful company at a fair price

than a fair company at a wonderful price – Warren Buffet

Let's face it, projecting cash flows into the distant future is about as fun as watching paint dry. That’s where Reverse DCF comes in. Reverse DCF is a valuation method that starts with an estimated terminal value and works its backward to determine if the stock is overvalued or undervalued. This approach is particularly useful when there is significant uncertainty about future cash flows, making traditional DCF projections challenging.

When you buy a stock, you trade cash for a portion of the future cash flows of a business. When you sell a stock, you trade the cash flows for cash. It’s a form of time travel: if you buy a stock at a price less than its perceived value, you are essentially traveling into the future and judging that today’s expectations for future cash flows are too low.

However, let us take a step back to look at the basics of this valuation technique. We will try to understand the traditional DCF Valuation method.

The DCF model is made up of several concepts, which are interwoven with one another. Naturally, we need to understand each of these concepts individually and then place it in the context of DCF.

The concept of future cash flow is the crux of the DCF model. However, since we are factoring today’s value of future cash flows of the business, the ‘Time Value of Money’ plays a crucial role. This means that money today is worth more than an identical amount of money in the future. Hence, we will have to evaluate what would be the value of money (cash flows) that we have today sometime in the future. We use a method called ‘Discounting’ to calculate the present value of money.

First, we look at the cash flow called ‘Free Cash Flows’ (FCF). The free cash flow is the excess operating cash that the company generates after accounting for capital expenditures. The mark of a healthy business eventually depends on how much free cash it can generate. Now, to move further in our process, we need to estimate the future growth rates of the cash flows and in turn the future cash flows. In most cases, we forecast the cash flows for 10 years (at least).

Next, we come to the concept of Terminal Value. This refers to the estimated value of a business at the end of a forecast period. It's a key component is used to capture the value of future cash flows beyond the projection period. So, we assign a Terminal Growth Rate to the cash flows beyond the forecast period. To calculate the terminal value, we just have to take the cash flow of the 10th year and apply the terminal growth rate.

Third, the Net Present Value. We use the free cash flows of next 10 years, and the terminal value and discount these values in today’s terms. We talked about ‘Discounting’ earlier and now we will apply the Discounting Factor to these cash flows to arrive at the Net Present Value of the company. The terminal value will be discounted by the 10th year’s factor. The summation of these two will give us the NPV of all future cash flows of the company. We can now adjust this figure with the Net Debt of the company to arrive at the Intrinsic Value of the company. This divided by the total outstanding shares will give is the value per share of the company.

We now come to the conversation of Reverse DCF. Reverse Discounted Cash Flow, is a financial analysis technique used to estimate the growth rate that a company's stock price implies. DCF is a valuation method that calculates the present value of a company's future cash flows by discounting them to their current value. In contrast, Reverse DCF involves using the current stock price of a company to estimate the implied future growth rate of cash flows needed to justify that stock price.

Rather than starting the analysis with an unknown, a company's future cash flows, and trying to arrive at a target stock valuation, we start instead with what you do know with certainty about the stock: its current market valuation. By working backward, from its stock price, we can work out the amount of cash that the company will have to produce to justify that price. If the current price assumes more cash flows than what the company can realistically produce, then we can conclude that the stock is overvalued. If the opposite is the case, and the market's expectations fall short of what the company can deliver, then we should conclude that it's undervalued. This information can be invaluable in identifying potential mispricing opportunities in the market.

Let's face it, projecting cash flows into the distant future is about as fun as watching paint dry. That’s where Reverse DCF comes in. Reverse DCF is a valuation method that starts with an estimated terminal value and works its backward to determine if the stock is overvalued or undervalued. This approach is particularly useful when there is significant uncertainty about future cash flows, making traditional DCF projections challenging.

When you buy a stock, you trade cash for a portion of the future cash flows of a business. When you sell a stock, you trade the cash flows for cash. It’s a form of time travel: if you buy a stock at a price less than its perceived value, you are essentially traveling into the future and judging that today’s expectations for future cash flows are too low.

However, let us take a step back to look at the basics of this valuation technique. We will try to understand the traditional DCF Valuation method.

The DCF model is made up of several concepts, which are interwoven with one another. Naturally, we need to understand each of these concepts individually and then place it in the context of DCF.

The concept of future cash flow is the crux of the DCF model. However, since we are factoring today’s value of future cash flows of the business, the ‘Time Value of Money’ plays a crucial role. This means that money today is worth more than an identical amount of money in the future. Hence, we will have to evaluate what would be the value of money (cash flows) that we have today sometime in the future. We use a method called ‘Discounting’ to calculate the present value of money.

First, we look at the cash flow called ‘Free Cash Flows’ (FCF). The free cash flow is the excess operating cash that the company generates after accounting for capital expenditures. The mark of a healthy business eventually depends on how much free cash it can generate. Now, to move further in our process, we need to estimate the future growth rates of the cash flows and in turn the future cash flows. In most cases, we forecast the cash flows for 10 years (at least).

Next, we come to the concept of Terminal Value. This refers to the estimated value of a business at the end of a forecast period. It's a key component is used to capture the value of future cash flows beyond the projection period. So, we assign a Terminal Growth Rate to the cash flows beyond the forecast period. To calculate the terminal value, we just have to take the cash flow of the 10th year and apply the terminal growth rate.

Third, the Net Present Value. We use the free cash flows of next 10 years, and the terminal value and discount these values in today’s terms. We talked about ‘Discounting’ earlier and now we will apply the Discounting Factor to these cash flows to arrive at the Net Present Value of the company. The terminal value will be discounted by the 10th year’s factor. The summation of these two will give us the NPV of all future cash flows of the company. We can now adjust this figure with the Net Debt of the company to arrive at the Intrinsic Value of the company. This divided by the total outstanding shares will give is the value per share of the company.

We now come to the conversation of Reverse DCF. Reverse Discounted Cash Flow, is a financial analysis technique used to estimate the growth rate that a company's stock price implies. DCF is a valuation method that calculates the present value of a company's future cash flows by discounting them to their current value. In contrast, Reverse DCF involves using the current stock price of a company to estimate the implied future growth rate of cash flows needed to justify that stock price.

Rather than starting the analysis with an unknown, a company's future cash flows, and trying to arrive at a target stock valuation, we start instead with what you do know with certainty about the stock: its current market valuation. By working backward, from its stock price, we can work out the amount of cash that the company will have to produce to justify that price. If the current price assumes more cash flows than what the company can realistically produce, then we can conclude that the stock is overvalued. If the opposite is the case, and the market's expectations fall short of what the company can deliver, then we should conclude that it's undervalued. This information can be invaluable in identifying potential mispricing opportunities in the market.

.webp)

When to Use Reverse DCF?

- Uncertainty about Future Cash Flows: When it is difficult to accurately predict future cash flows due to factors such as market volatility, economic uncertainty, or rapid industry changes.

- Quick Valuation: When a rapid valuation is needed and a detailed analysis is not feasible.

- Complementary to Traditional DCF: Reverse DCF can be used in conjunction with traditional DCF to provide a range of valuation estimates.

The key steps in a Reverse DCF are:

- Calculate the company's current free cash flow (FCF)

- Determine the forecast period and terminal growth rate

- Estimate the discount rate

- Calculate the terminal value

- Derive the implied growth rate that matches the current market price

By working backwards from the current stock price, the Reverse DCF technique removes

the uncertainty inherent in projecting future cash flows. If the implied growth rate is higher than what the

company can reasonably achieve, the stock may be overvalued. Conversely, if the market is pricing in a lower

growth rate, the stock could be undervalued.

Advantages of Reverse DCF Technique

- Eliminates the Need for Cash Flow Projections

- Gives Insights into Market Expectations (implied growth rates)

- Identification of Mispriced Stocks

- Useful for High-Growth and Volatile Companies

Limitations of Reverse DCF Technique

While useful, reverse DCF models have some

limitations:

- The method relies on current market price being efficient

- Assumes a constant growth rate over the forecast period

- Inherits most limitations of traditional DCF models

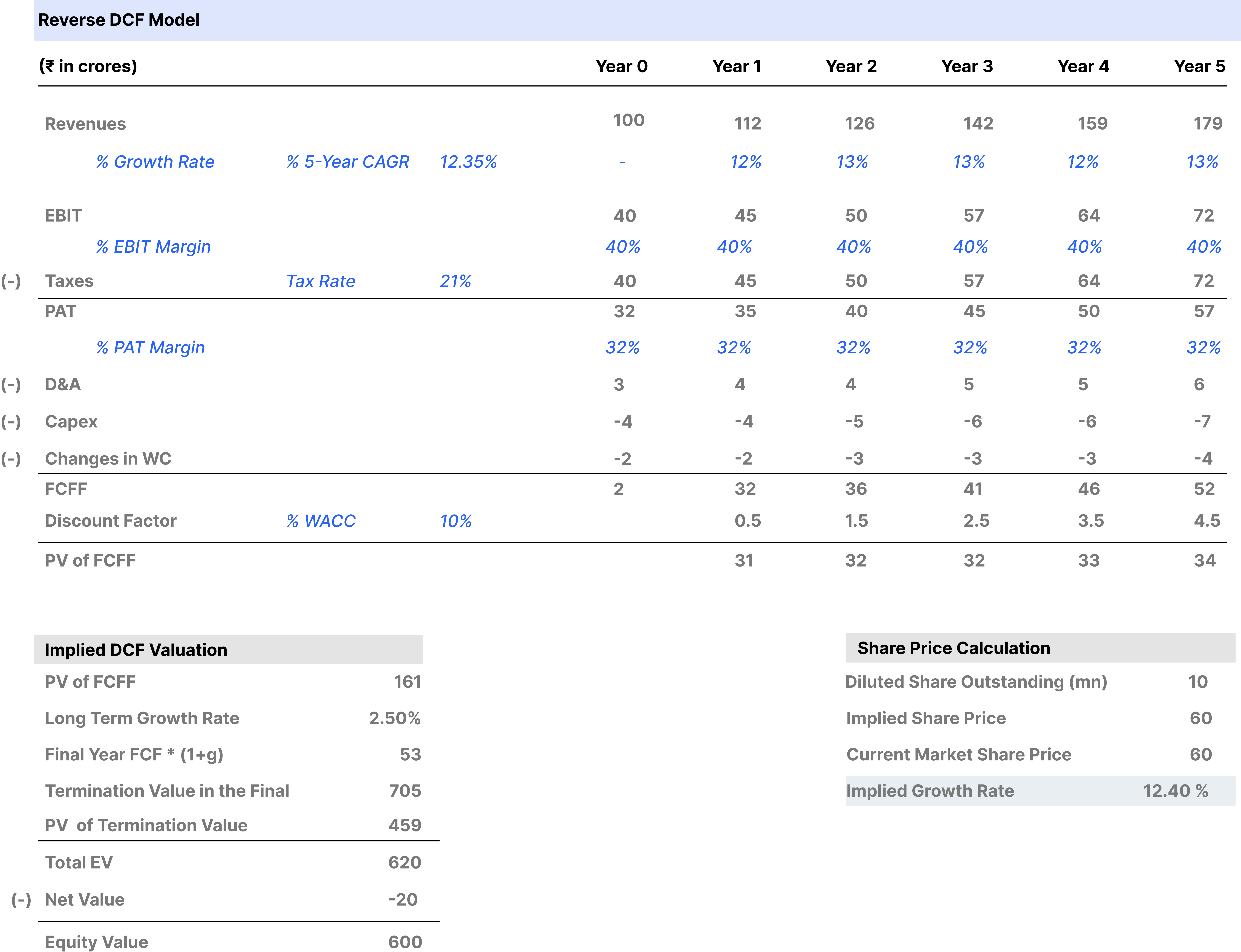

An example of the Reverse DCF concept –

Explanation of Each Step -

- Start with Current Stock Price: The process begins with the known current market price of the stock.

- Calculate Market Capitalization: Multiply the stock price by the total number of shares outstanding to determine the company's market value.

- Determine Current Free Cash Flow (FCF): Establish the current free cash flow, which serves as the base for future projections.

- Set Discount Rate: Choose an appropriate discount rate that reflects the investment's risk.

- Set Terminal Growth Rate: Define a terminal growth rate that will be applied beyond the forecast period.

- Adjust FCF Growth Rate Until PV = Market Cap: The core of the reverse DCF is iteratively adjusting the growth rate of future cash flows until the present value equals the market capitalization.

- Interpret Results: Finally, analyze whether the implied growth rate aligns with historical growth rates to determine if the stock is overvalued or undervalued.

Metal waste: Recycling rate for metal is between 20% and

25%.

- Total Ferrous Scrap Generated: 30 MT per year

- Recycled Ferrous Scrap: Approximately 9 MT (30% of total)

- Un-recycled Ferrous Scrap: Around 21 MT

Water waste: Only 28% of this wastewater is treated and

reused.

- Total Sewage Generated: 72,368 MLD (approximately 26.4 billion liters annually)

- Treated Sewage: 20,236 MLD (28% of total)

- Untreated Sewage: 52,132 MLD (72% of total)

E-waste: Approximately 33% of the total e-waste

generated

- Total E-Waste Generated: 1.6 million metric tons in FY 2021-22.

- E-Waste Collected and Processed: 0.527 million metric tons in FY 2021-22, representing 33% of the total.

- Recycling Rate: 33% of the total e-waste generated.

Municipal Solid waste (MSW): Approximately 75% is

processed.

- Total MSW Generated: 152,245 MT/day (~55.5 million tonnes/year)

- Processed Waste: 114,183 MT/day (~41.7 million tonnes/year)

- Recycling Rate: Approximately 75% of collected waste is processed.